Prices surge amid supply shortages; DRAM expected to jump 90 per cent in Q1 2026

Market observers note that this supply shortage reflects a strategic reallocation of global wafer capacity and memory chip prices are expected to climb further.

Nomura estimates that in Q1 2026, DRAM and NAND prices will rise by 90 per cent and 60 per cent, respectively, significantly higher than earlier forecasts of 56 per cent and 40 per cent. For the full year, commodity DRAM and NAND prices could reach 176 per cent and 146 per cent respectively.

The global memory market is currently dominated by Samsung, SK Hynix, and Micron Technology. According to Counterpoint Research, these three companies accounted for over 90 per cent of global DRAM market share in Q3 2025 – accounting for 33 per cent, 34 per cent, and 26 per cent respectively.

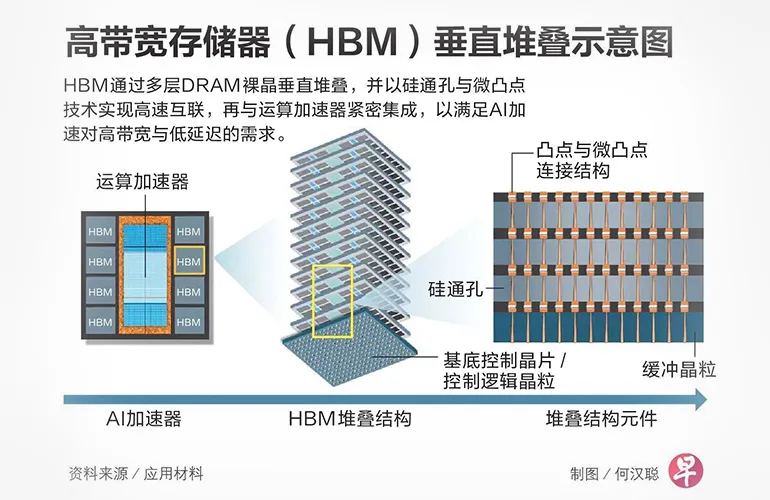

In HBM, their dominance is even more pronounced. SK Hynix holds 57 per cent, while Samsung and Micron account for 22 per cent and 21 per cent respectively.

Rising prices directly boost memory manufacturers’ profits. Nomura estimates that SK Hynix’s 2026 operating margins for DRAM and NAND could reach 76 per cent and 57 per cent respectively.

As AI customers race to secure supply, the latest generation of HBM – “HBM4” – commands even greater pricing power.

Nomura notes that while Samsung uses more advanced processes and faces higher production costs, high-speed versions of HBM4 could still command a premium of 30 per cent to 40 per cent amid the tight supply.

This has significant implications for everyday consumers.

Many research institutions believe that rising demand for high-end memory will crowd out production capacity for consumer electronics, as each wafer allocated to AI processors potentially displaces memory supply for smartphones and PCs.

As consumer electronics face rising cost pressures, consumer-oriented tech stocks have come under selling pressure – with Qualcomm, Nintendo, Logitech, and Chinese manufacturers BYD and Xiaomi among those feeling the strain.

Singapore: A major NAND production base

Maybank economists Chua Hak Bin and Brian Lee note that Singapore is a major global NAND production base. With Micron’s HBM chip plant and Taiwan’s United Microelectronics Corporation commencing local production, Singapore’s chip capacity and output is expected to increase, further cementing its position in the AI supply chain.

Notably, 98 per cent of Micron’s NAND flash chips are produced in Singapore. The company recently announced an investment of over S$30 billion to build Singapore’s first double-storey wafer manufacturing fab, which will create 1,600 jobs when it begins production in the second half of 2028.