Transition finance is expected to grow in Southeast Asia in 2026, following the release of international frameworks on how financing tagged with a sustainability label can be used by carbon-intensive sectors to facilitate their decarbonisation.

Late last year, the Loan Market Association published a guide on structuring transition loans aligned with net-zero pathways, while the International Capital Market Association released a similar tool for the issuance of transition bonds.

These guidelines are a “meaningful step forward” for Asian issuers, said Max Thomas, head of sustainable capital markets for Asia-Pacific at HSBC.

“The guidelines bring greater clarity on disclosures around transition strategy as well as addressing potential limitations or challenges to execution, providing a more holistic perspective to investors,” he added.

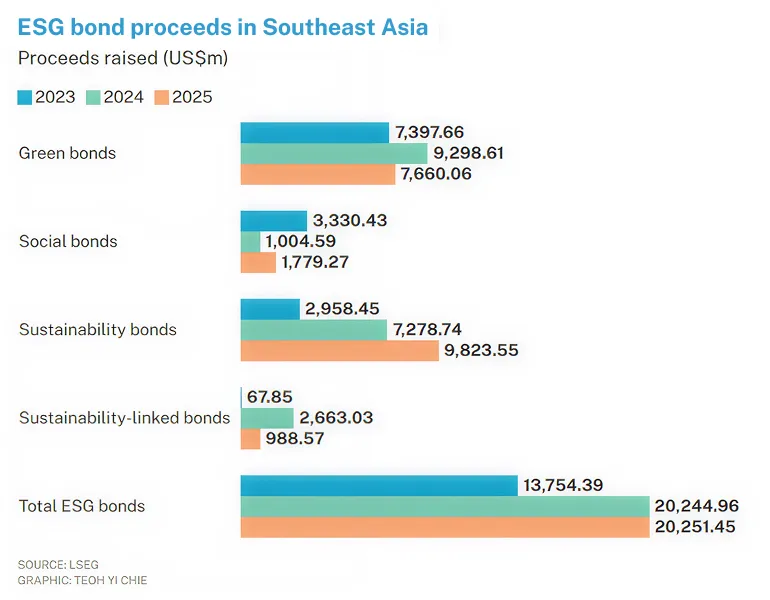

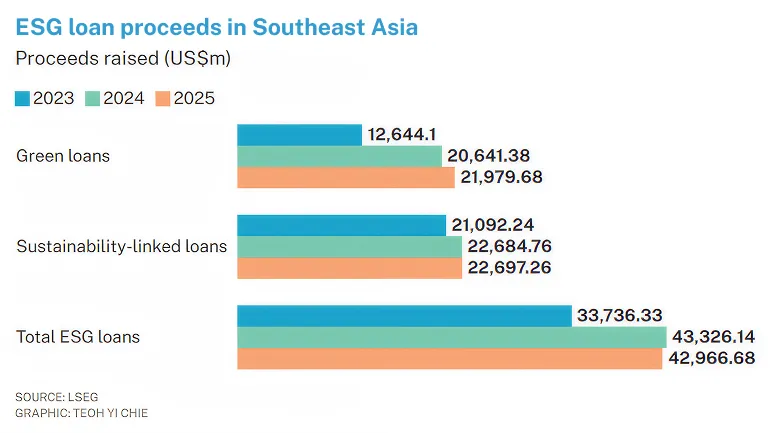

Sustainable finance proceeds raised in Southeast Asia remained flat in 2025, compared with the previous year, based on data provided by LSEG.

Proceeds from environmental, social, and governance (ESG) bonds came in at US$20.3 billion (S$26 billion) for the year, marginally higher than US$20.2 billion in 2024, as markets were hit with heightened risks and volatility due to tariffs imposed by the United States.

ESG loans slipped 0.8 per cent year on year to US$43 billion, from US$43.3 billion.

What to expect in 2026

While transition finance is not new, its growth has been stymied by the lack of standards and taxonomies that define credible transition. Sustainable finance taxonomies set criteria and thresholds for a range of economic activities that would be considered eligible for sustainable and transition financing.

Whether in the form of bonds or loans, transition finance has generally lagged behind its more common variants, such as green or sustainability-linked financing. Yet, hard-to-abate sectors have generally found it difficult to tap green financing as their carbon-intensive businesses do not meet the requirements.

That may soon change with the release of these two new international frameworks on transition finance.

In addition, the Singapore Sustainable Finance Association had also released additional guidance on how the Singapore-Asia Taxonomy can be leveraged for transition financing.

“Ongoing efforts to refine sustainable finance taxonomies, including the Singapore-Asia Taxonomy, for real-world usability will hopefully drive growth in this area,” said Jeong Yoonmee, head of global wholesale banking sustainability office at OCBC.

However, while transition bond and loan volumes are expected to grow, the lack of alignment across frameworks may still constrain volumes, said Martijn Hoogerwerf, head of sustainable solutions group for Asia-Pacific at ING.

“The market will closely watch upcoming issuances and how global taxonomies and standards are applied,” he added.