Across Southeast Asia, most countries have articulated net-zero or carbon-neutrality targets, signalling a clear collective commitment to the energy transition.1 However, translating these ambitions into implementation remains a structural challenge: how do we mobilise capital at scale, reduce risk, strengthen regional cooperation, and ensure the transition delivers both climate and development outcomes?

Using the United Nations Development Programme’s (UNDP) framework on innovative governance for private sector engagement, this article – through examining how Singapore supports the region’s energy transition by developing governance and financial frameworks to mobilise investment and strengthen collaboration – showcases how partnership-oriented governance and financial mechanisms can help align private incentives with public and regional development objectives2.

Energy Transition in Southeast Asia: A Structural and Development Challenge

Electricity demand in Southeast Asia has tripled over the past two decades, driven by economic growth, industrialisation, and expanded access to electricity.3 Yet this growth has largely been met through fossil fuels, particularly coal, which continues to account for around 45% of the region’s power generation.4 Although renewable deployment is accelerating, the pace of change remains insufficient to meet climate targets while supporting inclusive and resilient development.

These gaps do not stem from a lack of renewable resources or national ambition. Many ASEAN countries possess abundant access to renewable energy, such as solar, wind, and hydropower and have committed to net-zero pathways. The challenge lies instead in the fragmented grid systems, limited cross-border interconnections, and high financing costs.5 Together, these structural challenges raise project risk, undermine bankability, and lead to slow progress. These impacts are most acute in lower-income and emerging markets with limited fiscal headroom.

In contrast, Singapore has limited land and natural resources, but has strong regulatory institutions, deep financial markets, and policy credibility, which position Singapore well in the climate transition.6 This creates opportunities to move beyond isolated national approaches and towards cooperation built on complementary roles.

The International Energy Agency (IEA) has estimated that countries in Southeast Asia will need to double annual investment to nearly US$30 billion (S$38.4 billion) by 2035 to integrate renewable energy at scale.7 Meeting this need requires more than capital availability; it depends on mechanisms that reduce risk, improve coordination, and align private investment with public and regional priorities. Singapore’s contribution sits primarily at this enabling layer, consistent with UNDP’s emphasis on partnership-oriented governance.

Sustainable Finance as an Enabling Mechanism

Over the past decade, Singapore has developed sustainable and transition financing frameworks that correspond to the realities of Southeast Asia’s development pathways. The Finance for Net Zero (FinZ) Action Plan by the Monetary Authority of Singapore (MAS) marked a shift from a narrow focus on green assets, towards recognising the importance of financing credible transition activities, particularly in carbon-intensive sectors that remain central to many Southeast Asian economies.8

This approach is especially relevant for developing countries, where decarbonisation often involves gradual system transformation rather than immediate replacement. Financing frameworks that recognise transition pathways, while maintaining safeguards against greenwashing, can help unlock capital aligned with national climate transition priorities.

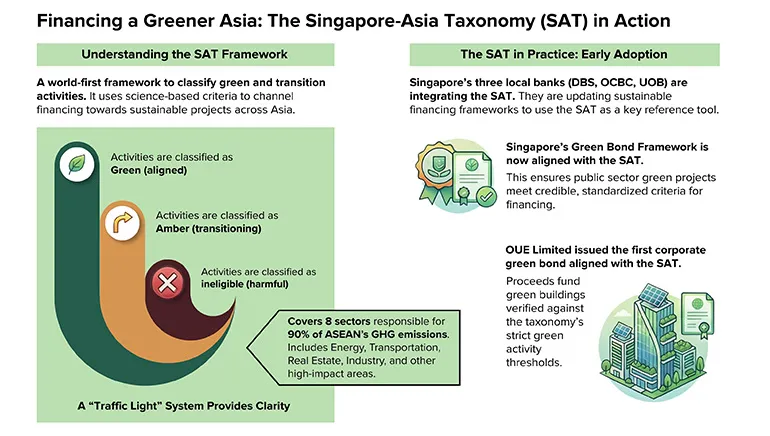

The Singapore-Asia Taxonomy for Sustainable Finance, the world’s first multi-sector transition taxonomy, provides a practical reference for classifying economic activities into green, transition, and ineligible categories.9 Its adoption at the regional level, including alignment with the ASEAN Taxonomy for Sustainable Finance,10 highlights how shared standards can reduce uncertainty for investors while respecting diverse national contexts.

These tools represent examples of direct policy actions that enable decarbonisation pathways in the region.