The region’s rich natural ecosystems and growing land-use pressures make Nature-based Solutions (NbS) a critical pathway for climate mitigation outcomes in Southeast Asia.

HAMERKOP’s recent analysis of Southeast Asia’s (SEA’s) NbS reveals that the region’s NbS carbon market is emerging with clearer regulatory signals, growing demand, and an expanding supply pipeline across Indonesia, Malaysia, Thailand, Cambodia and the Philippines. Under the mainstream international standards (VCS and Gold Standard), the region is a material contributor to the global NbS carbon market, having issued 129 million Voluntary Emission Reduction (VERs) (~22% of global NbS issuance) as of April 2025, with 43 million credits still available (~19% of global available supply), offering immediate procurement opportunities for corporates and traders.

There are three key insights on the supply and demand side market dynamics reshaping SEA’s NbS carbon landscape and commercial opportunities emerging from trends in issuance, availability, and future project pipelines:

1. Strengthening supply and emerging pipelines

With 43 million unretired credits and 28 projects under development across Indonesia, Malaysia, Cambodia and the Philippines, the region has great potential for global businesses committed to decarbonisation goals to secure credit supply whilst building early-stage project partnerships in SEA. At the same time, supply concentration plays a defining role in regional market dynamics. These countries currently dominate credit supply in SEA, together accounting for over 99.5% of all NbS credit issuance under the VCS and GS.

2. Increased credit retirement rate builds buyer confidence

The increase in credit retirement rates in the region from less than 20% in 2010 to over 65% in 2025, reflects stronger demand-side absorption and a greater willingness by buyers to use credits originating from SEA. In addition, the higher retirement rate for removal credits (≈12% above avoidance), creates opportunities for firms in carbon project development, MRV and low-carbon advisory. The limited supply of removal credits (≈0.01 million credits) also creates opportunities for project developers to scale reforestation and restoration NbS projects and for investors to secure early access to the high-integrity pipeline in SEA.

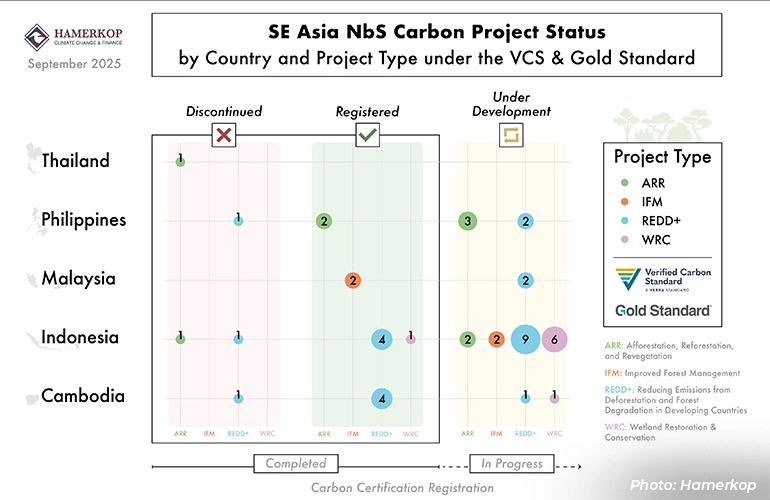

3. Project diversification expands market access

More NbS projects and a broader mix of project types e.g., Reducing Emissions from Deforestation and Forest Degradation (REDD), improved forest management, reforestation, etc. are emerging across SEA, reducing reliance on any single project category. This diversification helps buffer the region supply against regulatory changes or heightened scrutiny affecting specific project types, as well as potential supply bottlenecks for a certain project type. As a result, the region is better positioned to maintain a steady flow of credits to meet the heterogeneous preferences of global buyers with differing risk appetites, compliance considerations, and portfolio strategies. For example, beyond the REDD+ and Wetland Restoration and Conservation, Indonesia’s project pipeline has expanded to include ARR and IFM activities currently under development, broadening the range of options available to international buyers.

Singapore's position as a regional lighthouse—combining carbon market-friendly policies, conducive business environment, and proximity to SEA markets—makes it a natural base for firms seeking to capture these opportunities. With over 160 carbon services and trading firms available to provide their expertise, coupled with strong government support for climate finance, the country provides an ecosystem to support the region's growing NbS market.