Southeast Asia’s (SEA’s) carbon market has made progress in introducing comprehensive carbon market policies. To support carbon market activity, governments are operationalising their Nationally Determined Contributions (NDCs) through national registries and dedicated regulatory frameworks. As these policies mature, asset owners and carbon project developers will increasingly need to tailor their project development, financing, and technical approaches to align with specific national requirements. For businesses operating in carbon markets, this signals scalable market opportunities along the carbon services value chain, including advisory and technical services that support the sourcing, origination and financing of high-quality credits.

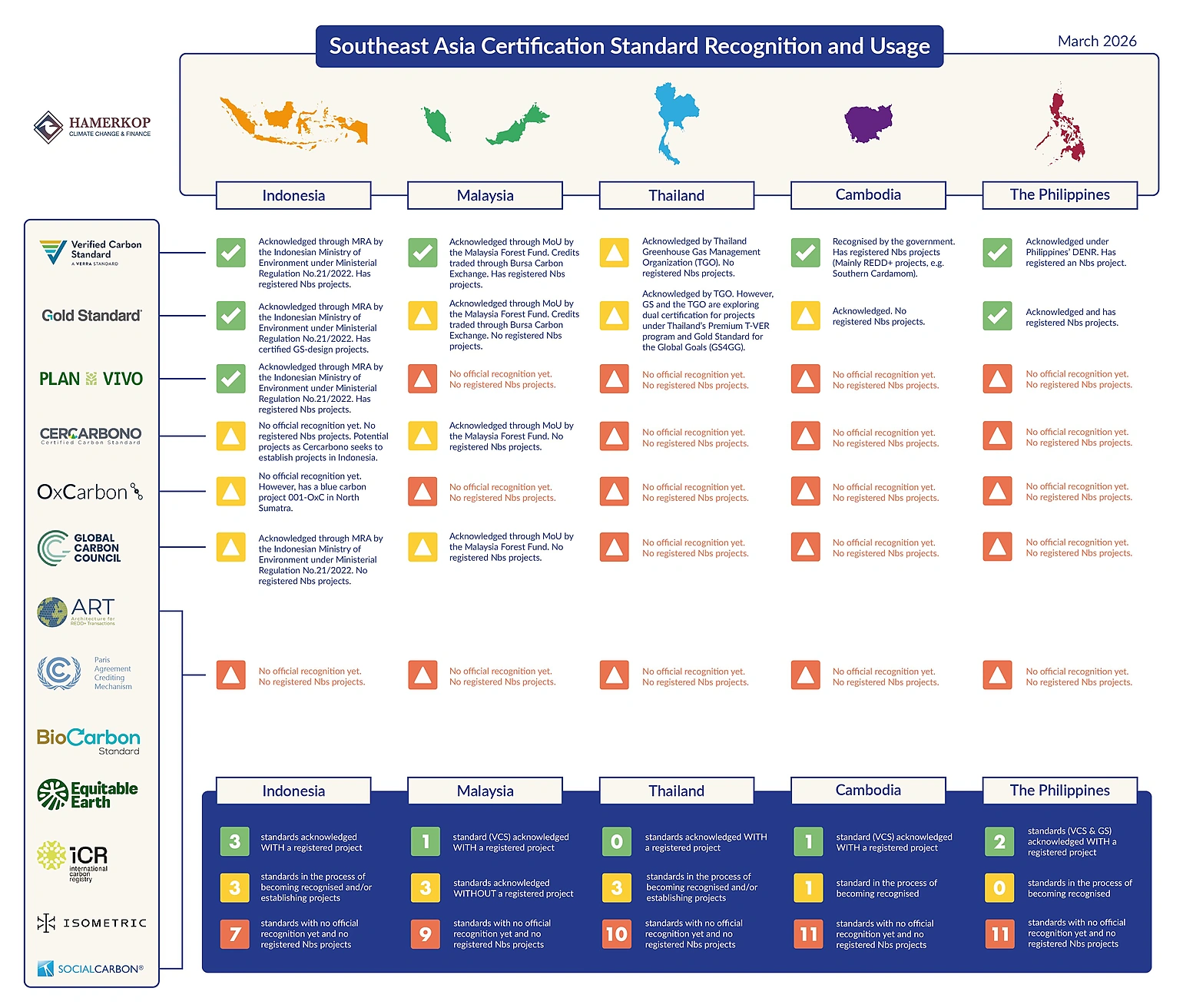

HAMERKOP analysed the landscape of 13 international certification standards for Nature-based Solutions (NbS) across Indonesia, Malaysia, Thailand, Cambodia and the Philippines, revealing a market characterized by varying regulatory maturity and a gap between policy recognition and on-ground implementation.

Their research reveals that the landscape is defined by three key trends:

1. Market dominance of established players

Activity is currently concentrated around the Verified Carbon Standard (VCS) and Gold Standard (GS). These standards hold a significant track record of registered projects and widespread recognition.

2. The SEA carbon market is diversifying and becoming more operational

Success for businesses and stakeholders depends on understanding not just the technical requirements of certification standards, but their political and regulatory compatibility with the host country’s specific climate strategy and policy landscape.

3. Recognition outpaces implementation

While many emerging standards are technically eligible or acknowledged in government frameworks, actual project registration trails behind. Actual activity clusters around a small set of the widely used standards, while niche standards are presently recognised but largely await first projects in most countries.

As SEA’s markets mature and regulatory frameworks become more sophisticated, demand for specialised advisory and technical services, spanning regulatory navigation, project structuring, market intelligence, and carbon certification, is set to grow. Singapore is well-positioned to serve as a regional hub for firms seeking to capture these opportunities. With an established carbon services ecosystem of over 160 service providers, strong government support for climate finance, and proximity to key markets in the region, Singapore offers a compelling base for companies looking to deliver high-value expertise across SEA's evolving carbon landscape.